What we heard on September 21st….

We kicked off the second day of the Global SME Finance Forum 2022 with Ruth Horowitz - Regional Vice President for Asia and the Pacific, IFC and his Excellency Phan Phalla - Secretary of State for the Ministry of Economy and Finance of Cambodia.

Both Ruth Horowitz and Secretary Phan Phalla spoke about the importance of digitalization in unlocking the potential of SMEs in so many economies. Secretary Phan Phalla spoke about Cambodia’s digital government policy plan (2022 – 2035) in which modernisation of public service delivery plays a big part to offer more concrete support to SMEs. He pointed out that fintech can have a big impact in the sector and the need for collaboration to achieve inclusive socioeconomic development.

They both also highlighted the potential shortcomings, stressing the risk that emerging technologies could deepen inequalities rather than ease them.

The first plenary panel of the day focused on leveraging digital innovations for women entrepreneurs and was moderated by Andrew McCartney – Senior Financial Sector Economist, ADB, joined by Debbie Watkins – CEO and Co-Founder, Lucy, Joyce Tee – Group Head of SME Banking, DBS, Khadija Mariam – Head of Women Entrepreneur Cell, BRAC Bank and Rachel Freeman – Executive Director, Business Development, Tyme.

Panelists shared how digitalization facilitate innovative and effective products and solutions so that more women entrepreneurs become better and more deeply “banked”. Debbie, Joyce, Khadija and Rachel gave us the benefit of their experience and passion for tailoring digital services to women.

Following this panel, we were privileged to be joined by Her Excellency Chea Ratha, Under Secretary of State of the Cambodian Ministry of Industry, Science, Technology & Innovation (MISTI) whose remit includes working to develop resilience, inclusive SME policies, and Building a Strategic Framework to Engage and Empower Women in the Digital Economy.

It was exciting to hear from her about the Cambodian government’s interest in leveling the digital playing field through policy and action. As we know, a supportive and intelligent regulatory ecosystem is important for digitalization to occur at a pace and reach that lifts all boats and not just some.

After those panels, we moved into a breakout session titled credit bureaus leveraging digitalization. We had the pleasure to hear from Joe Bowerbank – Business Development, Creditinfo, Robert Grimberg – CEO, TREFI, Tony Hadley – EVP, Experian and Rajeev Chalisgaonkar (moderator) – Head of Business Banking, Mashreq Bank.

Panelists raised interesting points about how credit bureaus can use new sources of lender’s data as digitization increases their capabilities to create more comprehensive lender profiles.

Tony looked into the future and said that data analytics will grow ever more important. He believes consumer education & financial literacy offer up a lot of opportunities to credit bureaus. Joe also believes that the combing of data sets will bring more opportunities for innovation. This all ratchets up the urgency for proper stewardship of the data. Regulatory frameworks are really important to maintaining trust in any burgeoning consumer centric models and ensure the quality and validity of the data. Rob pointed to progress in Peru in creating the holy grail of invoicing data by preparing to set up an institution through which all credit invoices will flow and to which credit bureaus will eventually have access.

Our first panel of the afternoon tacked achieving and sustaining green finance. It was moderated by Francisco Avendano – Senior Operations Officer, IFC joined by Bruno Laskowsky – Director of Capital Markets and Indirect Credit, BNDES, Edoardo Borsari – Managing Director, Strands, Ivana Tranchini – Country Manager for Cambodia, Visa and Oskar Miel – Managing Partner, Rakuten Capital

The panelists laid out the opportunities of a “Twin Transition”: digitalization that also accelerates a green revolution.

Ivana stated that small businesses are doing their best to deliver value to their customers, and the role of the banks is to come in and facilitate that process.

One way is to partner with each other (banks and fintechs) so that data can be shared, and customers can get a more integrated experience of financial services as a whole.

Typically, when there is a transaction on the fintech’s platform, there’s a collection and movement of data. This data is often very impressive and can offer banks precious insight. Partnerships can also help us track the movement of carbon: from the way it is being produced to when it is being offset.

To Oskar, ESG is still a bit opaque. It’s still unclear what constitutes compliance to ESG values. Oskar spoke of a start-up who partnered with Rakuten called ‘Proof of impact’ that measures the ESG compliance of a company and whose assessments are being taken into consideration by credit providers. One of Rakuten Capital’s most successful loan portfolio is called Upstart. They use a different point of data coming from the social chain of people’s ability to pay and don’t look at the traditional score of the banking agency. This has effectively provided more inclusion and more access to funding.

Francisco flagged up IFC’s efforts to support members’ creation of ESG taxonomies.

He also highlighted the importance of finding technological ways to encourage reduction in the huge losses in water and energy caused by crop spoilage or losses. He wants to see more decarbonisation embedded in products.

“Electricity metric in Brazil is 85% renewable”, stated Bruno. Brazil is a nation with a tremendous opportunity in becoming one of the main actors in the green economy, especially in offshoring carbon credit. Currently, the world produces up to 60 billion tons of CO2 and Europe, the US, and China make up more than 60% of the share while Brazil only takes up 2% of the total carbon emission. However, in terms of the carbon credit reserve, Brazil was said to have taken up a share of 15 to 20%. The financial system in Brazil is extremely strong, efficient, and highly technological. On the other hand, 85% of the credit, especially for SMEs, is run by only 5 banks. Diversification in the credit market is needed in order to foster competition.

Edoardo highlighted that for developing countries to get into green finance, which is highly associated with digitalization and data collection and usage, setting up the foundation is key. The very first step is to build the right infrastructure and get all key players, especially the central banks, to be involved. One good example he raised is the case of Madagascar who wants to develop an analytical solution for providing credits. However, in doing so, they need to have 12 to 18 months of data to make the prediction or analysis. Therefore, an infrastructure that collects and stores data effectively will need to be put in place to enable this technology.

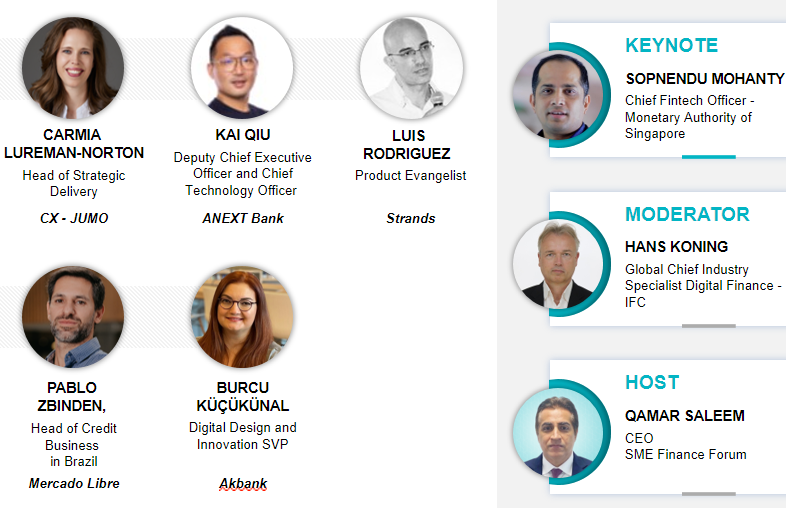

The final panel of the conference revolved around the future of SME payment infrastructure. Panelists H.E. Dr. Chea Serey – Assistant Governor, National Bank of Cambodia, Carrie Suen – Senior Advisor, International Public Policy and Government Affairs, Ant Group, Manu Rajan – Division CEO, Wing Division, Jay Singer – SVP for Global SME Product Development, Mastercard and moderator Matt Gamser - CEO, SME Finance Forum explored an impending payments revolution that could significantly change the landscape for SMEs.

H.E. Dr. Chea Serey explained that registration of SMEs is a good step towards identifying a small business, but it is not enough because it doesn't show the business performance: type of product, export, client, supplier, and sales revenues. If SMEs stay out of the formal system, this kind of data is hard to capture. She stated: “In Cambodia, we promote electronic payment because we want to create some digital footprint for SMEs to help financial institutions better serve them”.

“To encourage people to go into the digital payment space, you must make the digital payment easy. And to make it easy, it has to be cheap, fast and convenient.” In Cambodia, the Bakong technology is the latest generation of mobile payments and baking platform initiated by the National Bank of Cambodia for a peer-to-peer fund transfer service available to retail customers of local banks, financial institutions, and payment service providers in Cambodia.

To increase the level of adoption of digital payment, the two main issues are digital and financial literacy. First, how do we make sure SMEs know what to do with the money they can seek now and second, how do we ensure that the customers trust the sellers and pay the sellers beforehand, so-called “upfront payment”, so that the SMEs can use this as a working capital instead of taking out loans from banks to use as their capital.

H.E. Dr. Chea Serey noted that once digital payment is adopted, the government could work on installing a system that gives access to the business’s operation, through a general ledger that can record all transactions (in particular for tax purposes).

Manu explained that Cambodia is a country with one of the cheapest data (internet) in the world. From his perspective, data connectivity is not the problem in Cambodia for getting people onboard with digital payment.

Carrie introduced AliPay which started in 2004 as a payment function on Alibaba in order to build trust between people when doing online purchases. Currently, Ant Group is focusing on getting SMEs ready for the next space of growth after the pandemic: how to get consumers to increase their transactions successfully and have SMEs engage with customers more directly. Another focus is on building a cross-border solution to bring digital wallet into cross-border. They are currently working with Singapore and looking to bring other countries like Thailand and Malaysia into the system.

Jay explained that businesses don’t only focus on the payment, but the core activities of the business itself. Cards are not the only form of payment. Since payment can be made through other ways such as using crypto currency or e-wallet, Mastercard’s role as a payment method provider is to find ways to integrate these different methods and to allow customers to choose their own payment methods. To create such connected platforms, Mastercard focuses on three main things:

Making sure the platforms are stable: focus on security and trust

Extending into crypto while investing in authentication and tracing fraud.

Finally, to get more people onboard with digital payment, education and capacity building are important tools to reduce the barriers.

Jay concluded “I have talked to some of these small businesses, they don’t care about how businesses operate, or more importantly, they don’t understand all these challenges. Therefore, anything you do, has to be simple, it has to be solving issues so clients can transact, manage their data and information safely and securely, helping them grow their business. Simplicity is the key, education is critical.”

The closing remarks of the Global SME Finance Forum 2022 were given by Piyush Gupta – CEO, DBS

Piyush was not able to join in person but shared his thoughts in this video

Conclusion by Georja Calvin-Smith – Event Emcee

During this year’s conference, we have seen that digitalization can be a powerful tool to improve conditions for SMES of all sorts:

- enabling the inclusion of women and other marginalized and unbanked populations

- can have a big impact in cutting back global carbon emissions by reducing the amount of resources used in a given sector

- can help empower individuals and businesses through data availability and analysis and an adapted regulatory framework

But technology can also exacerbate the very problems it seeks to address, so anticipation and assessment of unintended consequences are important in making sure that digitalization is equitable and that as much as possible, mitigating actions can be taken when and where needed to maximise the positive difference they can make and minimise the harm.

Throughout these conversations we’ve heard calls for banks to do more to walk the walk when it comes to changing their organisational mindsets in investing more in the potential of SMES. That needs new ways of thinking and new ways of reaching out. Also raised was the importance and potential in partnering with the growing number of visionary fin tech companies, in order to get a closer, alternative insight into SMEs data and creditworthiness. Doing so can more easily marry capital to solutions and perhaps even birth more healthily empowered SME offspring.

Overall, though there is almost boundless potential to leverage technology to make impactful human connections.