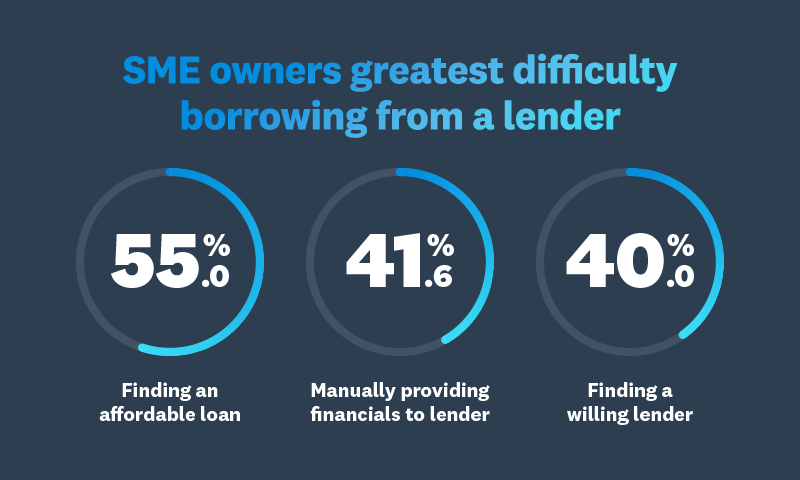

Oliver Wyman and Fundera surveyed small business owners in late 2016 to better understand the preferences, behaviors and experiences of this segment. The research identified several areas in which lenders of all types fall short of what borrowers told researchers they want. Borrowers said that the search and application processes are complicated and time consuming, loan pricing and terms are difficult to understand, and comparison shopping is arduous because it requires multiple applications and comparison of inconsistently presented offers. These largely unaddressed customer needs create opportunities for lenders to differentiate themselves.

In addition, the research confirmed FinTech lenders perform better than banks in creating a satisfying borrowing experience, across factors like application length, communication of next steps, and time to approve loan applications. Indeed, borrowers from traditional institutions were about twice as likely to be frustrated by these aspects of the application process as borrowers from alternative lenders. However, alternative lenders’ high cost of funds leads to higher pricing that frustrates borrowers. If alternative lenders begin to develop stable, low cost funding sources, banks might need to shore up their relative weakness across most elements of customer experience. Even if this threat does not materialize, banks should want to invest in customer experience improvements to gain an advantage over their peers.