Blog

Tarun Sridhar

Matt Gamser

Member Pulse Survey #4 on the Impact of COVID-19 - July

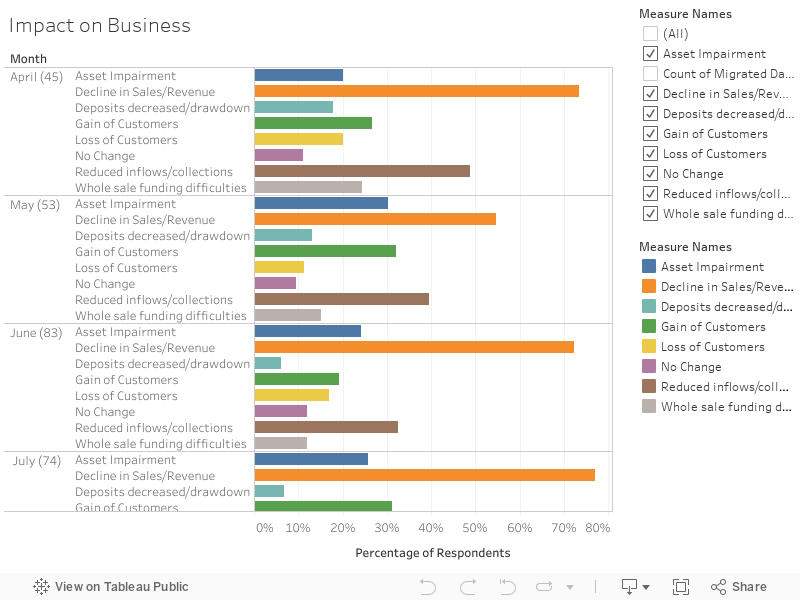

Once again, a significant number of members responded to our monthly pulse survey (76). We’d like to thank our members for their continued support! Last Thursday, at our Virtual Roundtable session, after the preliminary breakdown of the survey responses, we discovered that for the first time most respondents reported from Sub-Saharan Africa (26%) rather than Europe & Central Asia (20%). This shift may explain some changes in the survey results. Further analysis will be conducted to ascertain if the type of institution or region was a key influencing factor in the responses.

Last month, we introduced a new sample of consistent, month-on-month respondents to be able to provide different comparative view of trends. Since May, we have had 30 consistent respondents. While it is a small sample and not externally valid, it offers an alternative perspective.

We are seeing a decline in members reporting Reduced Collections. Conversely, there is an increase in members reporting Gain of customers (+12%). To a lesser extent, since last month, more members are also reporting a Decline in Sales and Loss of customers (+5%), exceeding April’s numbers.

The repeat respondent sample parallels the changes in Gain of customers (+16%) and Reduced collections. It moves in the opposite direction is apparent for Loss of customers and Decline in Sales (-8% and -9% respectively). It has fewer members reporting Wholesale funding difficulties (-8%) and Asset impairment (-10%) than the overall sample. Could this mean this group feels more on the path to recovery? We need to wait a few more months on this.

More members’ operations are affected by COVID19 (51% reported limited closure), with fewer reporting they are not affected. There is also an increase, on average, in mandatory and voluntary moratoria timelines for loan repayments.

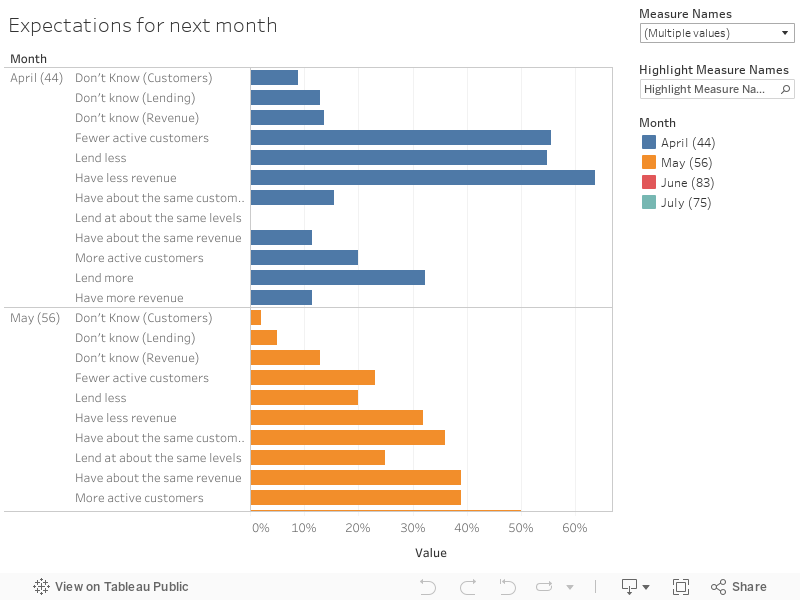

There is a consistent trend of optimism about next month’s business (revenue- +7%, customers- +10%, and lending- +9%) and about the resiliency of their SME clients. Over 80% (+7% from June) of our respondents expect less than 40% of their SME clients to be in distress in three months.

Our repeat respondents share the increased optimism, especially on lending and the health of their SME clients.

Viewing our data month on month, sentiment, on average, is less gloomy – how much of this is due to real resilience and recovery, and how much is due to just getting used to new arrangements is difficult to say.

Only more time will tell, particularly when government relief programs conclude, whether this is Stockholm syndrome (hostages getting more comfortable in a terrible environment) or legitimate optimism.

Share with us other insights you can derive from the data!