Blog

Tarun Sridhar

Member Pulse Survey 2021 Q2 on the Impact of COVID-19

Sep 15, 2021

In February 2021, we launched our revised pulse survey, to be run quarterly, with more targeted questions to understand how our members, and by proxy how their SME clients, are faring. We had 71 respondents working in 143 countries, out of which 47 are lenders working in a little over 100 countries.

Our second round of surveys this year, during the period of June/July, saw 104 respondents working in over 192 countries. In addition, as part of our work with the Italian Presidency of the G20’s Global Partnership for Financial Inclusion, five new questions regarding the extent of digitization of our members were added.

Staff Operations

The current sample of members, similar to that of February, mostly remain affected by limited closures (58%). The good news is that a significant portion of respondents with physical operations continue to report that their staff have been at least somewhat effective (98%) working from home. Many reported that their staff were completely effective (53%), keeping in line with February’s respondents (56%).

Impact on Business

Some 50% reported an increase in sales/revenue. This is coupled with a continued drop in members reporting a drop in sales/revenue. There also seems to be a downward trend in members reporting Asset Impairment. Otherwise, we see a consistent proportion of respondents saying they are facing liquidity challenges (i.e., Wholesale funding, Deposits decreased, Reduced collections).

Customer Behavior

Some 90% of our respondents with physical operations say there has been a shift in customer behavior. More members report a medium-high proportion of digital sales origination compared to February’s results. The proportion of customer digital activity remains stable from February.

We continue to see increases in customer use of digital channels like Smartphone Apps and (75%), Websites (68%), as well as more use of Call Centers (67%), with a continuing decrease in use of Branch Offices (57%) . Most respondents continue new investment in IT (though fewer members (72%) compared to February (92%)). A good number continue to and reallocate resources to IT (59%) and to invest (61%) in Product Design. About half still say they are investing in Customer Service improvements.

Most respondents continue to say that this shift in resource allocation will be permanent.

Lending

The majority still say that their portfolio has been negatively affected (66%). However, we see a slight increase in members reporting only a slight negative impact (41% to 54%) rather than a significant one (26% to 11%), and more members reporting a positive impact on their portfolio (11% to 20%)

Similar to February, more than half of these respondents say their time from loan application to onboarding has stayed the same, with only a few reporting that it has decreased (25%). However, fewer than in February (18%) say it has increased.

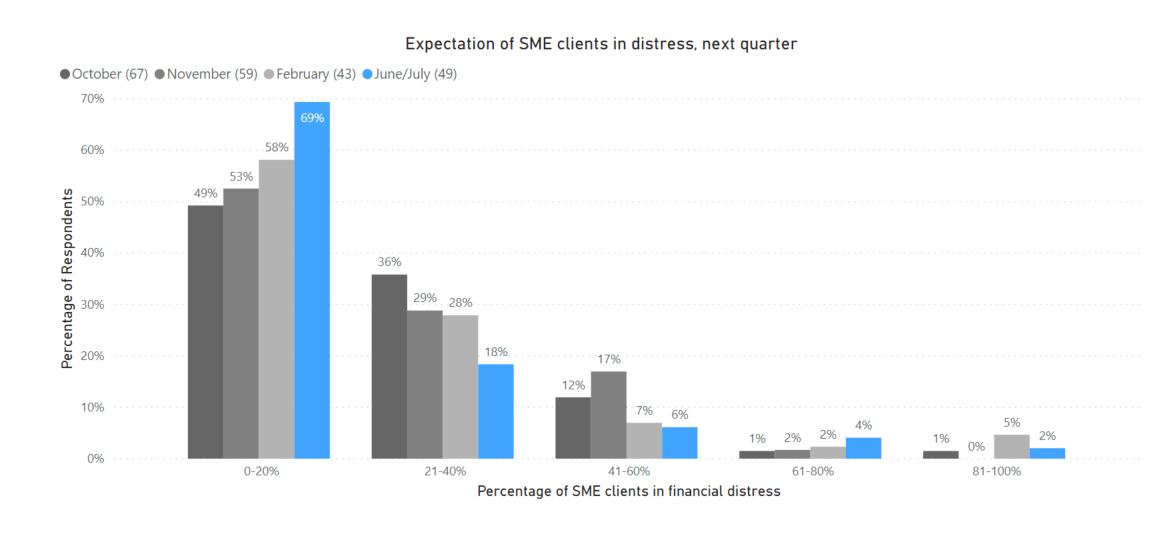

Almost all respondents say they are continuing lending to existing and new customers. Most (84%) report they are lending to new customers mostly in existing sectors. We are also seeing continued improvement in the situation of our members’ SME clients – Most (70%) say that fewer than 20% of their SME clients are in financial distress as of now, a big improvement from 18 months ago. Respondents also are more optimistic about the future prospects for their clients, and about how their lending volumes and customers numbers will grow over the next quarter.

Digitalization

Finally, regarding the extent of digitization, we see that some operations have adapted quicker than others. A significant majority of the respondents say that their payment services have been fully digitized. Fewer than half say their loan applications and processing services have been fully digitized. Insurance seems to be falling even shorter, with only one member reporting having fully digitized this operation.

Most members report that COVID-19 has pushed them to adopt API technology (73%), and to a lesser extent, AI/ML (53%) and cloud computing (51%). Few (17%) reported adopting Blockchain/DLT. A significant number say that they have partnered or are considering partnership with a Fintech.

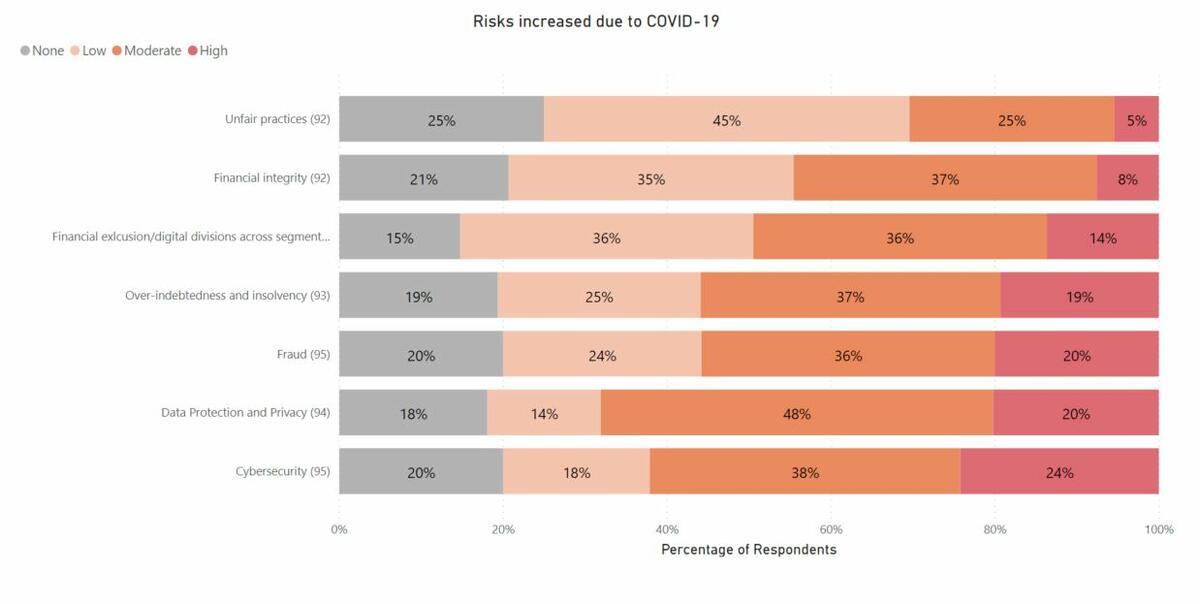

Finally, while digitization has its benefits/opportunities of reach and efficiency, members are cognizant of new risks this brings. In this area, new risks most cited were Data protection and privacy (68%), Cybersecurity (62%), and Fraud (56%), Over-indebtedness and Insolvency (56%) rated as a moderate/high increase in risk as a result of COVID-19.

What do you make of this data? What questions do you have? Feel free to reach out and let us know!

Read full report here>