Blog

Diego Del Pilar

Data Story: The importance of supporting MSMEs during the pandemic

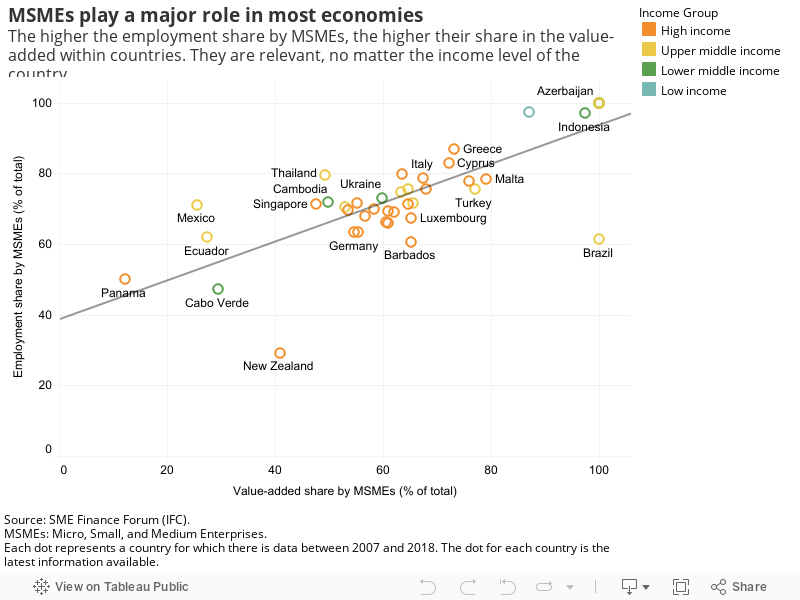

Micro, Small, and Medium Enterprises (MSMEs) play a significant role in most economies. According to the World Bank, they represent about 90% of businesses and 50% of employment worldwide. In emerging markets, most formal jobs are generated by SMEs, that is, seven out of ten posts. They are essential as well in production terms since they make between 50% and 60% of the value-added on average, in OECD countries, and they contribute up to 40% of the GDP in emerging economies.

See the interactive visualization below.

The ongoing COVID-19 pandemic is putting at risk a critical percentage of SMEs around the world. The OECD stresses that the current crisis has affected SMEs disproportionately, and it has revealed their vulnerability to the supply and demand shock, with a severe risk that over 50% of SMEs will not survive the next few months. A collapse of SMEs would imply job losses, consumption and demand fall, and potential financial risk due to an increase in the non-performing portfolios that can generate systemic effects on the banking sector.

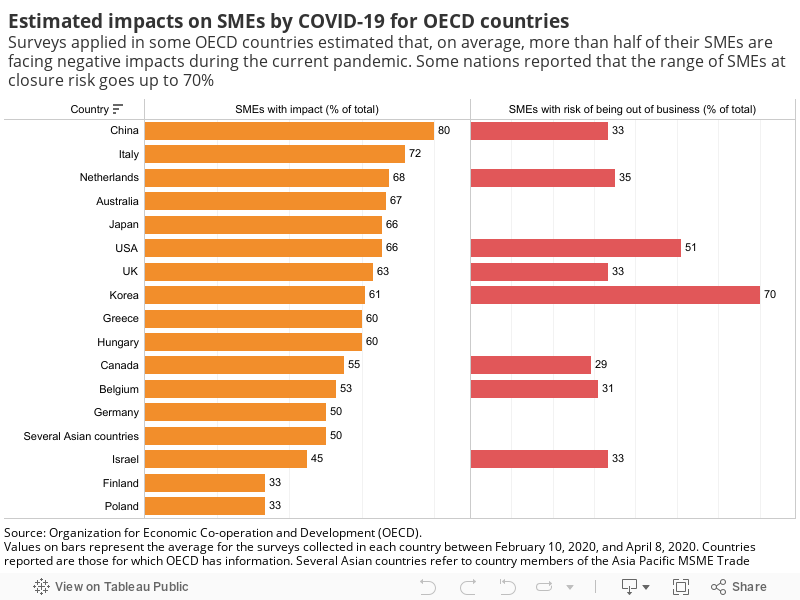

A compilation of surveys made by the OECD for its country members about SMEs' affectations, highlights that more than half of SMEs already face severe losses in revenues. Without further support, one-third of SMEs fears to go out of business within one month, and up to 50% within three months. Magnitude and types of impact vary [1] across countries; for example, Finland and Poland reported that one-third of their SMEs are facing a negative impact, while 80% of Chinese ones are affected.

See the interactive visualization below.

In the United States, a recent NBER paper (Bartik, et al., 2020) [2] presented the results of a survey of over 5,800 small businesses, showing that 43% of responding enterprises are already temporarily closed. On average, companies reduced their headcount by 40%. Three-quarters of respondents indicate they have two months or less in cash reserve.

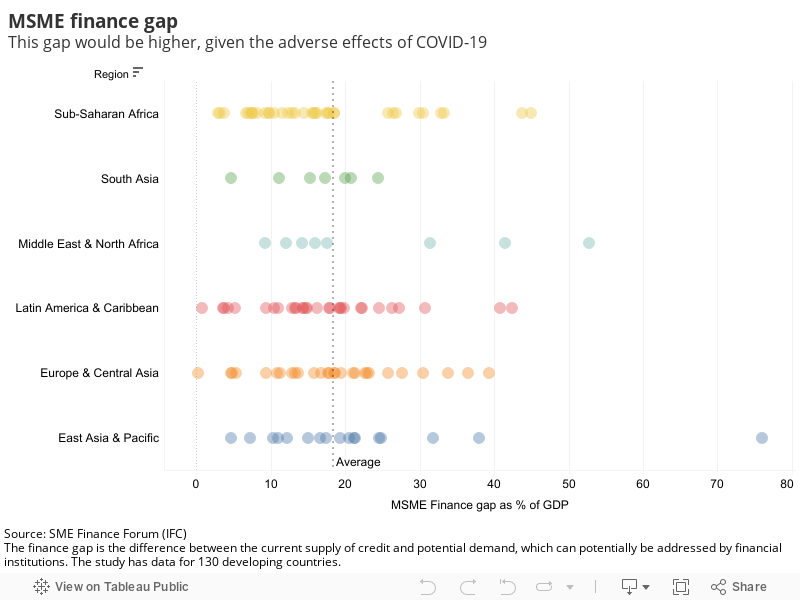

Affectations for SMEs in developing countries would be as severe as in developed countries, aggravated by the lack of access to finance. The International Finance Corporation (IFC) estimates that 65 million firms, or 40% of formal MSMEs in those countries, have an unmet financing need of $5.2 trillion every year, which is equivalent to 1.4 times the current level of the global MSME lending. This finance gap, defined as the difference between current supply and potential demand, which could potentially be addressed by financial institutions, represents on average 18% of the GDP of developing countries.

See the interactive visualization below.

Given the sort of effects that MSMEs are facing, most governments are implementing credit programs to support their liquidity needs, avoiding closures, and anticipating their financial needs once the economies re-open. Due to the narrowness of fiscal space in some developing nations, boosting access to finance could be the difference between cushioning the crisis or letting it get worse. In the end, supporting SMEs means supporting workers.

This story was developed by Diego del Pilar Miranda, with information extracted from the SME Finance Forum Data Sites.

Contributors: Marie-Sarah Chataing (Communications Lead), Khrystyna Kushnir (Knowledge Management Lead), and Carina Carrasco (Web and Social Media Editor)

References:

[1] Impacts reported include halted operations, supply disruptions, decrease in sales, increasing cost, cash flow problems, and planning lay-offs.

[2] Bartik, A. W., Bertrand, M., Cullen, Z. B., Glaeser, E. L., Luca, M., & Stanton, C. T. (2020). How Are Small Businesses Adjusting to COVID-19? Early Evidence from a Survey. NBER Working Paper. Retrieved from https://www.nber.org/papers/w26989.pdf

#COVID19 #Data #SMEs