Blog

Mohan Chen

How COVID is accelerating partnerships between big tech and banks

This is a virtual roundtable summary.

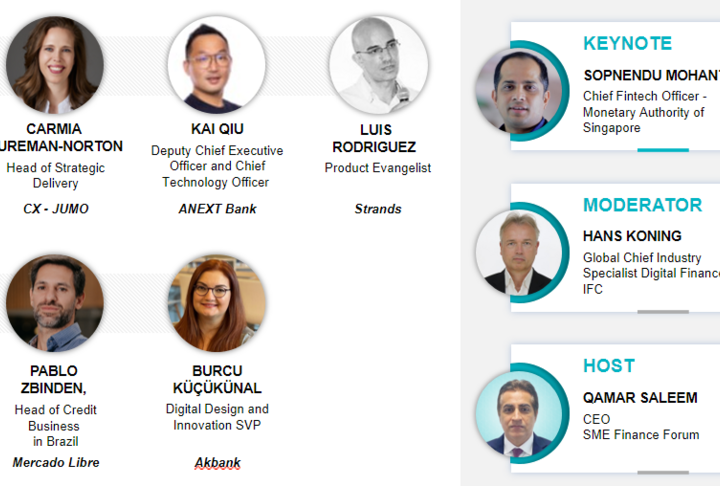

The pandemic has brought several changes to the SME Finance ecosystem worldwide. Many banks and Big Tech companies chose to partner together to provide solutions to counter the challenges posed by COVID-19. This roundtable aimed to examine the increasingly important role of Tech Giants in the SME financing arena. With their experience in other fields, including social networking, e-commerce, and supply chain purchasing, the large players are working with or competing against the established traditional financial institutions in the SME financing industry. Ankur Mehrotra (Grab), Tunde Kehinde (Lidya), Bing Xiao (Wells Fargo), Juan Lopez Carretero (BBVA), and Facundo Cuppi (Mercado Libre) participated in the panel to discuss the potential partnerships and competition between Big Tech companies and banks in the post-COVID era.

Over the past year, COVID-19 has reshaped the SME financing sector by stimulating both competition and partnerships between Big Techs and banks. Bing Xiao, the Senior Vice President of Wells Fargo Small Business Lending, believes that the pandemic has motivated corporations to change in two major ways. First, the banks have become more eager to utilize technology to accommodate their customers. For example, the U.S. government has established a $995 billion COVID relief program, Paycheck Protection Program (PPP), to provide small businesses with the necessary resources that they need to maintain their payroll and cover other expenses. By May 2021, the lenders had distributed $800 billion to almost 12 million small businesses, which means the total number of applications was even much higher. Hence, it was critical for the banks to deal with such a huge amount of loan applications online and accelerate the decision-making process with the aid of technology. The ‘new common’ has made the traditional financial institutions realize the possibility of reform as well as the importance of investing in innovations. Secondly, many fintech companies have also been persuaded to partner with banks rather than becoming banks themselves throughout the pandemic. As business closures and loan delinquencies for COVID-19 impacted businesses were anticipated to increase significantly in the United States, the fintech companies came to the realization that there are many downsides to have balance sheets and they lack experience or loan reserve as banks to weather such situation. There will be more partnerships between banks and Big Techs overall after the pandemic, Xiao concluded.

Ankur Mehrotra is the Managing Director and Head at Grab, the number one super app company offering food delivery, transportation, and digital financial services in Southeast Asia. The financial services at Grab have four major components: e-wallet, lending and credit solutions, insurance, and asset management. Mehrotra shared insights from the fintech perspective. When the pandemic hit the region in March 2020, Grab Financial Services was growing at a tremendous rate. The company initially decided to hold back some investment while not pulling back completely from the market. In addition, Grab built a “COVID playbook” in case of lockdowns and moratoriums, which they still refer to until now. In terms of partnering with banks, the scenarios and strategies vary in each jurisdiction. Grab has open partnerships with the banks across the region in general and has been willing to work closely with financial institutions through risk sharing programs, such as co-lending. Mehrotra has also witnessed the increasing openness from the traditional financial sector in Southeast Asia to partner with fintech companies and explore digital channels over the past few years. Currently, many banks have turned to new approaches including leveraging fintech companies’ existing user journey to acquire new customers. And in a market where more than 60% of the population is underbanked or unbanked, the financial institutions need new ways to assess the credit of individuals or SMEs to make better loan decisions.

Juan López Carretero from BBVA also shared his opinions towards the future of partnerships between banks and Big Tech companies. It is important to understand that not every small business or region is equipped for the digital transformation accelerated by COVID-19. BBVA has seen uneven states of readiness among its clients in different countries, which exposed several weaknesses. As a universal bank, BBVA has encountered a number of challenges induced by the pandemic throughout the processes of their traditional banking activities. For example, the bank needs to find ways to evaluate the credit of clients with thin profiles. López Carretero stated that COVID-19 has enabled the banks to identify who are prepared for the “new economy,” thus determine the developmental strategy for geographies in distinct situations. On the other hand, the pandemic encouraged the traditional financial institutions to adapt to the “new reality” by cooperating with tech companies. A rising number of consumers have been moving from physical venues to cyberspaces for shopping or other business activities, consequentially, it becomes desirable for the banks to partner with e-commerce platforms. To accomplish meaningful partnerships, the banks should first review all the execution processes and their engineering capabilities. For instance, the institutions need to have APIs that work seamlessly with the new technologies and mature protocols that prevent digital frauds.

Tunde Kehinde, the Co-Founder of Lidya, commented on the trajectory of partnerships between Big Techs and banks that have been formed over the pandemic. the partnerships targeting to provide small businesses with COVID-19-related solutions have gradually come to an end. However, Lidya, a data-oriented fintech that provides access to credit and finance across frontier and emerging markets, has initiated a new phase of discussion with its clients and partners. Because of the pandemic, many institutions realized that they are not yet ready to move forward with digitalization and determined to invest more in long-term initiatives, such as payments, KYC, insurance, and credit. Due to the sense of urgency or lack of technological capability, these financial institutions often seek support from the tech companies to help them achieve a smooth digital transition in the medium and long terms. In addition, there are a lot of discussions around finance and embedded finance by non-banking partners, who would like to introduce credits and payments into their ecosystems to ensure value chains in the post-COVID times. Hence, the partnerships between banks and Big Techs will last beyond the pandemic and thrive with new focus in the future.

Facundo Cuppi, the Director of Strategy & Operations for the lending business at Mercado Libre, shared his insights as an e-commerce industry leader. In Cuppi’s opinion, the most important in a successful partnership is trust. The participants should be transparent and communicate thoroughly in order to understand each other’s objectives and plans. In the case of Mercado Libre, Cuppi pointed out that the banks should have a clear perception of their products as well as their development strategies. This way, the financial institutions can be flexible in accommodating the e-commerce company’s growing portfolios and changing approaches that are dependent on the market to a great extent. The second key to success is technology gap. Most traditional financial institutions lean on mainframe-based propriety banking systems, which are inaccessible to external entities. To increase the probability of seamless integration, it is important for the banks to devise a new ecosystem that is easier for the tech companies to work with.

In conclusion, the pandemic has incentivized both Big Tech companies and traditional financial sector institutions to collaborate to address the issues that small businesses have been facing. And this partnership is projected to be an inevitable trend that will last in the “new normal.” To ensure a meaningful partnership, the two sides need to hold an open attitude and establish shared objectives.