The European Central Bank’s latest semi-annual survey on business financing, released November 30, registered further improvement in the financial situations of Euro Area SMEs and their access to finance. For the fourth consecutive six-month reporting period, Q2/Q3 2016, more SMEs reported bank credit more available and at lower interest rates than reported the opposite. This was in line with quarterly surveys of bank lenders, the ECB noted, confirming a favorable trend in credit supply for Euro Area SMEs. The results reflected positive effects both from the ECB’s liquidity support measures, especially the targeted long-term refinancing operations (TLTROs) begun in 2014 and Juncker Plan guarantees for bank loans to SMEs, launched in 2015 and extended with doubled funding in late 2016.

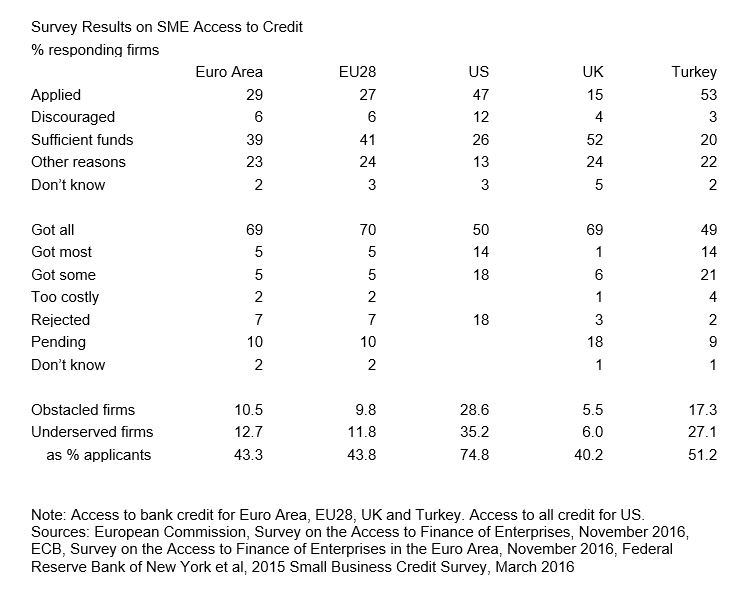

Reduced numbers of rejected credit applications have helped lower the share of underserved SMEs, including those rejected in full or in part, discouraged from applying for fear of rejection or choosing to turn aside high interest credit offers. Counted in this way, underserved SMEs amounted to a still high 43% of applicants in the latest survey, down from a peak of 63% in the Q4 2013/Q1 2014 survey. As a share of all SMEs, however, underserved firms still remained high at 20%, including firms seeking credit from nonbank lenders. This was down from a 28% peak in Q4 2013/Q1 2014 but little changed from the preceding six-month period.

The ECB prefers a narrower estimate for firms seeing obstacles to bank credit, including only firms experiencing or fearing rejection, getting only some rather than most of credit requested or turning away credit offers deemed too expensive. On this measure, 10.5% of surveyed SMEs faced credit obstacles in April-September, slightly less than in Q4 2015/Q1 2016. While adding responses about credit from nonbank lenders to those about bank credit risks double counting those firms interested in both forms of credit, even the smaller figure still amounted to 36% of firms applying for bank credit, a number that increases marginally to 38% adjusting for pending applications and don’t know responses and including firms reporting that they received most rather than only some of requested credit. Either figure underscores the extent to which SMEs’ principal external financing channel remains impeded in the Euro Area despite the extraordinary measures taken by Frankfurt and Brussels. The same ratio was somewhat worse for applicants for nonbank credit, standing at 42% and pointing to the challenge to be faced developing alternatives to bank credit.

How much these figures differ from similar measures in the US and UK depends on which surveys one uses. The broadest and most recent measure for the US, done by a number of regional Federal Reserve banks for 26 eastern states in the final quarter of 2014 and the first three of 2015, reported that 47% of small businesses had applied for credit. This was close to the 46% total in the latest ECB survey derived by summing applicants for bank and nonbank credit. Larger numbers of discouraged and rejected borrowers in the US survey left the number of underserved SMEs at 75% of those applying for credit. The large number of applying firms compared with the Euro Area increased the share of underserved firms to 35% of reporting SMEs, nearly double the total in the latest ECB survey, adding together applicants for both bank and nonbank credit.

Different reporting in the UK points to a much smaller number of credit applicants with high approvals rates, especially on credit renewals. Even so, the latest survey by the UK Federation of Small Business records 39% of respondents reporting poor or very poor credit availability in Q4 2016, a marked improvement from a peak of 62% in Q4 2014 but increased from the previous quarter. The most recent figure was still nearly three times larger than the 14% of UK SMEs applying for credit then, according to the FSB survey. A different picture arises for the 600 or so firms UK SMEs included the latest EU28 survey by the European Commission, which was done at the same as the Euro Area survey by the ECB. Only about 6% of UK SMEs in the EC survey saw obstacles or were underserved on the definitions set out above. Very low numbers of firms applying for bank loans, however, mean that underserved SMEs amount to 40% of applicants, not far off the Euro Area figure, and close to the latest FSB figure on poor or very poor credit availability.

Part of the reason for both the low numbers of applicants and the low numbers of discouraged nonapplicants in the EU figures for the UK could be the vibrant market there for online and marketplace lenders. Despite growing rapidly, however, new SME lending by alternative lenders has yet to exceed 5% of that done by UK banks. Data for Turkey, also reported by the European Commission, show Turkish SMEs near their US counterparts in terms of numbers applying and applications met in full but with fewer discouraged and rejected borrowers. The result is a share of underserved firms closer to the US relative to all reporting SMEs but nearer the situation in the Euro Area as a share of credit applicants.

http://ec.europa.eu/growth/access-to-finance/data-surveys_en

Jeffrey Anderson is a Senior Advisor for the SME Finance Forum, responsible for membership solicitation and policy advocacy on issues connected with access to finance for SMEs. He was previously with the Institute of International Finance, where he directed economic and financial analysis for emerging Europe and the Euro Area periphery and led a well-received study conducted jointly with Bain & Company on impediments to small business finance in the Euro Area.